Don’t miss our content

SubscribeOn April 14, 2025, the European Parliament approved the Stop-the-Clock Directive, one of the regulations included in the Omnibus I Proposal published by the European Commission, which aims, among other objectives, to simplify sustainability reporting and corporate due diligence regulations.

Below, we explain this directive’s objectiveand its benefits for companies.

Context: towards general simplification of EU regulations and administrative procedures

In the strategic plan presented in January—the EU Competitiveness Compass—the Commission recognized that the “regulatory burden has become a brake on Europe’s competitiveness”.

To address this situation, the Commission committed to, among other measures, reducing companies’ reporting obligations by 25% (raising this threshold to 35% for SMEs) and relieving the administrative burden. On February 26, 2025, the Commission presented its first simplification proposals, including the Omnibus I Proposal which aims, among other things, to ease sustainability reporting and corporate due diligence regulations.

For more details, see Post | The EU Competitiveness Compass and the first omnibus proposals.

Objective of Stop-the-Clock Directive: give greater legal certainty to companies

The main objective of this directive—that forms part of the Omnibus I Proposal—is to give companies more time to adapt and meet the sustainability regulations that are under review, without incurring unnecessary costs.

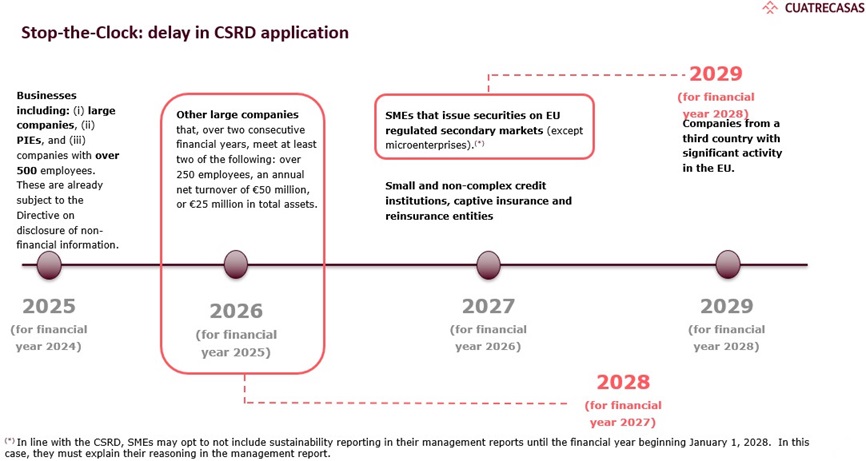

Postponing CSRD Directive reporting obligations

There is a delay period of two years in applying the reporting requirements under the Corporate Sustainability Reporting Directive (2022/2464/EU)—the "CSRD Directive"—for:

- large companies due to report in 2026 (for financial year 2025), which will now have until 2028 to do so (for financial year 2027); and

- listed SMEs due to report in 2027 (for financial year 2026), which will now have until 2029 to do so (for financial year 2028).

NOTE: Click on the image to enlarge.

Postponing transposition deadline and application of CS3D Directive

- There is a delay in the transposition deadline of the Corporate Sustainability Due Diligence Directive (2024/1760/EU)—the “CS3D Directive”—until July 26, 2027.

- Application of the regulations has been postponed by one year—until July 26, 2028, instead of July 2027—for the largest companies. This includes companies with over 5,000 employees and a net annual turnover of over €1.5 billion. For the other two company groups, the schedule does not change.

What are the next steps?

This directive will enter into force the day after its publication in the Official Journal of the European Union and its transposition deadline ends on December 31, 2025.

Once the Stop-the-Clock Directive has been approved, negotiations will continue on other proposals from the Omnibus I package. These could introduce substantial changes to the CSRD Directive’s scope of application, its requirements, and the CS3D Directive and the taxonomy regulations. For more details, see Post | The EU Competitiveness Compass and the first omnibus proposals.

Conclusion

Cuatrecasas's appraisal of the Stop-the-Clock Directive is positive given that, by postponing compliance deadlines, companies will:

- have more time to adapt to the regulatory framework arising from the Omnibus Proposal I, and have greater legal certainty to assess the adjustments they may need to make to their sustainability policies and strategies; and

- avoid incurring unnecessary expenses, and therefore be able to allocate their resources to business activity in a complex geopolitical and digital transformation context.

For more information, please contact our Knowledge and Innovation Group.

Don’t miss our content

Subscribe